Credit risk assessment of expressway listed company in China

Article Text (Baidu Translation)

-

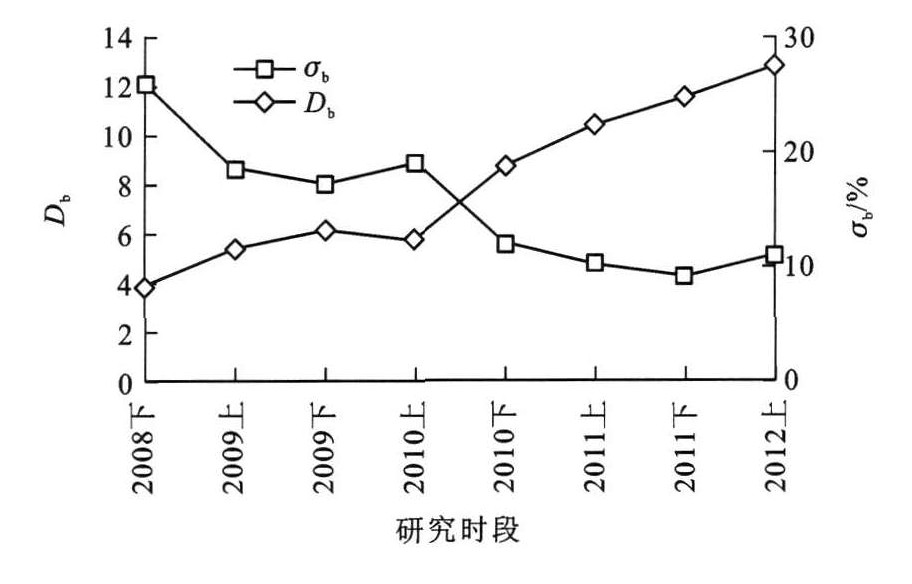

摘要: 以16家中国高速公路上市公司为样本, 研究了金融危机对高速公路经营企业信用风险的影响。运用KMV模型计算了样本公司自2008年下半年至2012年上半年的半年度违约距离及其变化趋势。计算结果表明: 在研究区间内, 违约距离以20.11%的平均增长率逐步增加, 信用风险不断降低, 信用风险水平与中国GDP半年度增长率和高速公路板块指数的Spearman相关系数分别为-0.012和-0.381, 不存在显著的相关性, 信用风险受企业资产市场价值波动率的影响大于流动负债水平的负面影响, 中国高速公路上市公司仍然具有较高的投资价值。Abstract: In order to research the impact of financial crisis on the credit risks of expressway enterprises, 16 expressway listed companies in China were chose as samples, the half-year default distances of the companies from the second half of 2008 to the first half of 2012 were calculated by using KMV model, and the changing trends of credit risks were analyzed.Calculation result shows that default distance increases with an average growth rate of 20.11%, and the credit risk decreases gradually. The Spearman's correlation coefficients between the credit risk and China's half-year GDP growth rate and expressway sector index are -0.012 and -0.381 respectively, so the inherent correlations are not significant. The influence of the volatility of enterprise's market value on the level of credit risk is greater than the negative influence of the level of current liability. Expressway listed company in China still has high investment value.

-

Key words:

- traffic economic and management /

- expressway /

- listed company /

- credit risk assessment /

- KMV model

-

表 1 样本公司基本信息

Table 1. Basic informations of sample companies

样本公司 上市时间 所处地区 发行股票 股票代码 除权股价/元 每股净资产/元 净资产收益率/% 资产负债率/% 湖南投资 1993 湖南 A 000548 4.53 2.97 1.78 29.99 东莞控股 1997 广东 A 000828 5.52 3.09 5.92 35.94 海南高速 1998 海南 A 000886 3.46 2.61 2.91 12.20 现代投资 1999 湖南 A 000900 9.19 13.65 5.82 26.05 山东高速 2002 山东 A 600350 3.40 3.45 5.67 31.51 华北高速 1999 北京 A 000916 2.99 3.61 3.52 5.98 皖通高速 2003 安徽 A+H 600012 4.03 3.72 6.09 38.83 宁沪高速 2001 江苏 A+H 600377 5.51 3.50 6.71 32.28 赣粤高速 2000 江西 A 600269 3.74 4.48 6.21 53.43 粤高速 1998 广东 A+B 000429 3.04 3.34 3.77 60.61 楚天高速 2004 湖北 A 600035 3.17 3.51 4.12 68.53 重庆路桥 1997 重庆 A 600106 3.66 2.16 5.40 63.26 五洲交通 2000 广西 A 600368 3.93 3.19 7.02 71.02 福建高速 2001 福建 A 600033 2.36 2.58 3.33 56.17 深高速 2001 广东 A+H 600548 3.71 4.25 4.48 56.54 中原高速 2003 河南 A 600020 2.46 2.87 2.47 79.07  下载: 导出CSV

下载: 导出CSV

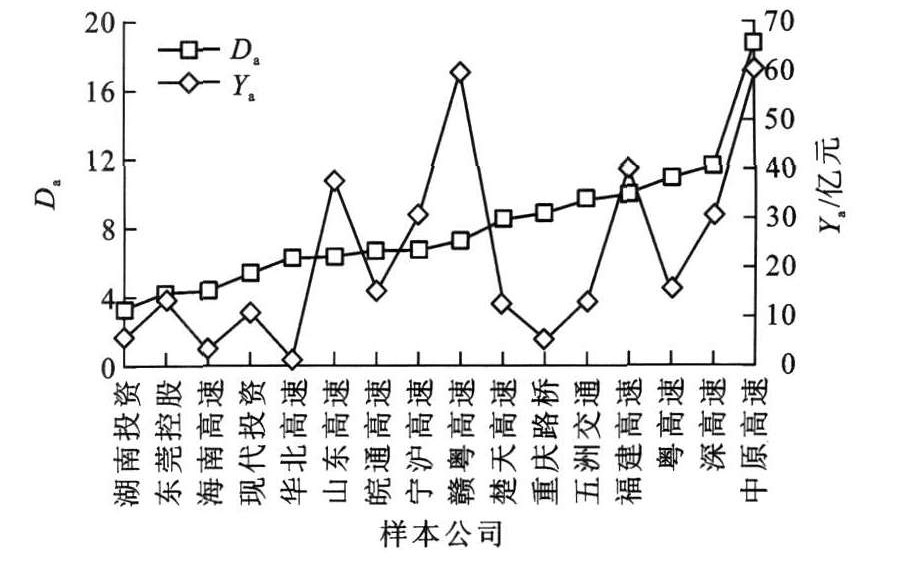

表 2 违约距离

Table 2. Default distances

样本公司 2008年 2009年 2010年 2011年 2012年 Da 下半年 上半年 下半年 上半年 下半年 上半年 下半年 上半年 湖南投资 2.037 9 2.419 8 3.112 2 3.221 8 4.080 6 3.642 4 4.868 1 3.007 1 3.298 7 东莞控股 1.917 4 2.636 2 3.482 9 3.437 4 4.168 2 7.085 6 5.869 7 5.661 9 4.282 4 海南高速 3.035 3 3.648 0 2.994 8 2.168 6 6.604 2 6.001 3 5.129 1 5.467 5 4.381 1 现代投资 3.225 6 4.203 4 5.302 8 4.129 6 5.855 6 6.588 3 7.700 3 6.298 0 5.412 9 华北高速 3.215 5 2.463 3 5.521 2 5.079 4 7.708 0 9.042 0 7.839 9 9.387 0 6.282 0 山东高速 3.213 3 4.481 2 5.576 2 5.964 8 7.517 1 10.612 4 8.957 3 4.559 4 6.360 2 皖通高速 3.177 9 4.220 8 7.327 3 3.580 2 4.180 2 6.329 4 10.318 7 14.486 8 6.702 7 宁沪高速 3.848 8 5.248 8 5.762 4 3.780 4 6.932 8 5.615 1 9.948 5 12.993 0 6.766 2 赣粤高速 3.264 6 6.113 4 2.918 9 5.195 5 7.156 8 10.111 3 10.559 3 12.882 8 7.275 3 楚天高速 3.093 1 4.741 4 5.732 4 3.799 5 5.353 7 10.238 3 14.917 4 20.708 8 8.573 1 重庆路桥 5.683 7 10.209 9 7.985 9 7.485 3 12.680 3 14.406 4 7.859 2 4.839 0 8.893 7 五洲交通 2.385 0 4.858 9 5.225 3 3.736 4 12.374 7 12.767 0 16.059 6 19.943 6 9.668 8 福建高速 4.745 8 6.448 7 6.566 3 4.978 7 9.748 6 14.433 9 15.618 5 17.226 3 9.970 9 粤高速 5.347 5 7.245 9 8.639 6 10.840 9 11.409 9 9.482 8 16.248 6 18.417 8 10.954 1 深高速 4.712 7 6.957 5 8.782 5 11.993 8 11.242 8 12.440 4 11.144 0 25.792 6 11.633 3 中原高速 8.522 3 9.887 4 13.266 1 12.797 8 23.298 1 27.219 2 31.545 9 23.292 5 18.728 7

下载: 导出CSV

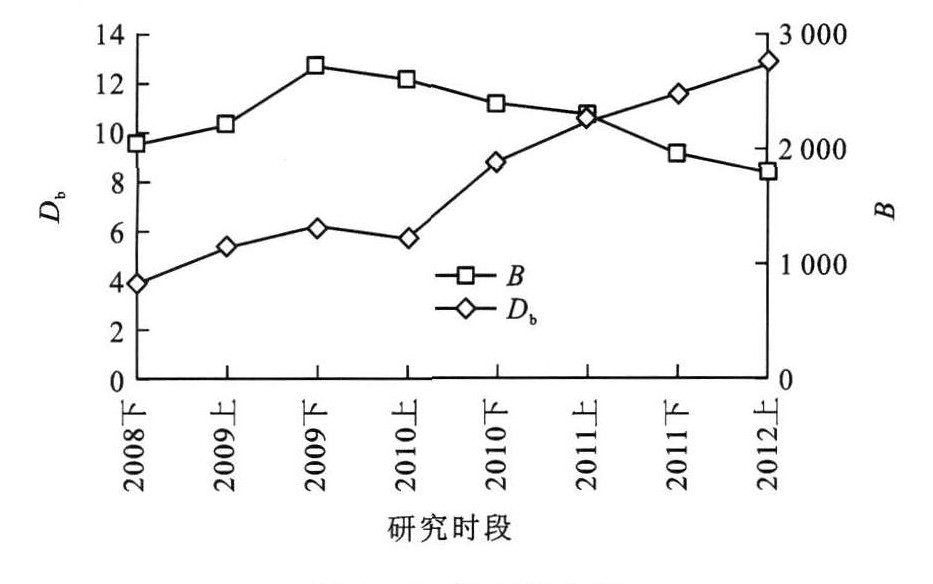

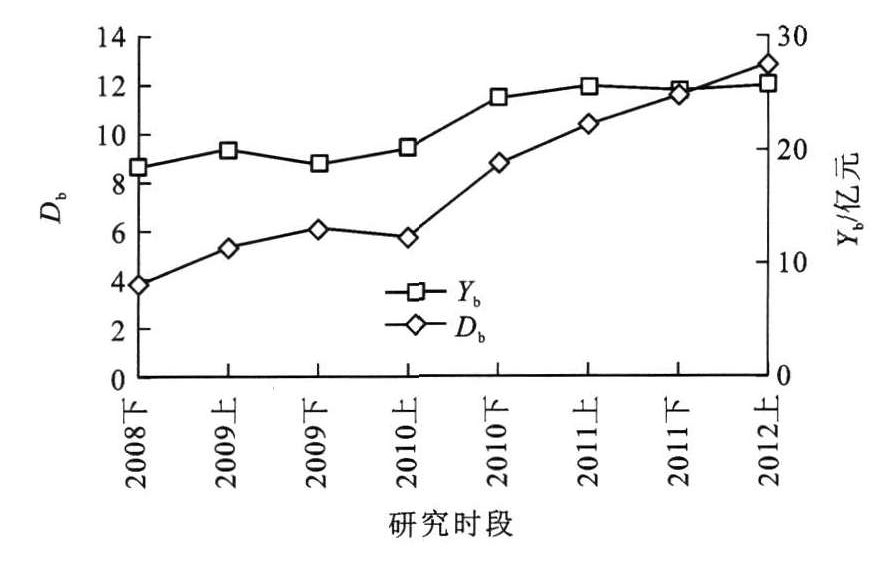

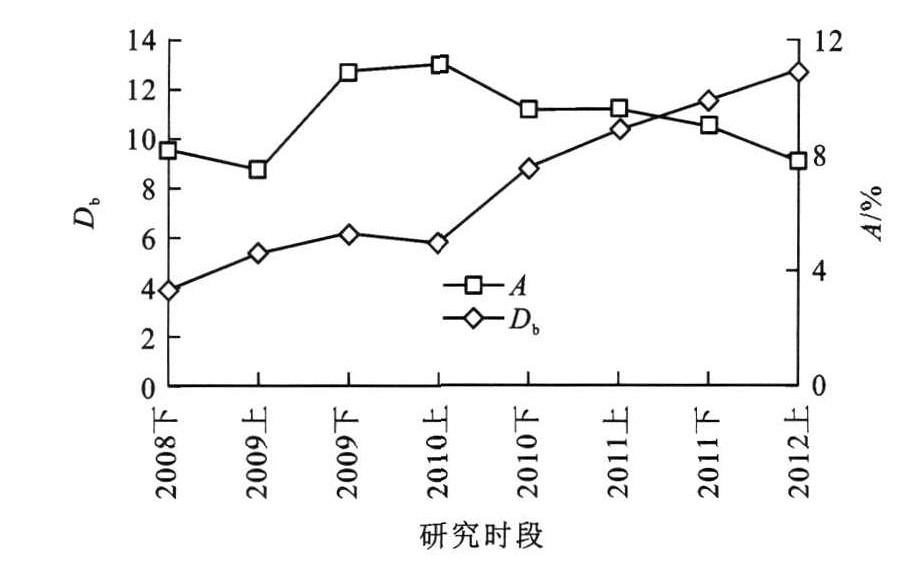

表 3 违约距离均值、GDP增长率及板块指数

Table 3. Average default distances, GDP growth rates and sector indexes

研究参数 2008年 2009年 2010年 2011年 2012年 下半年 上半年 下半年 上半年 下半年 上半年 下半年 上半年 Db 3.839 2 5.361 5 6.137 3 5.761 9 8.769 5 10.376 0 11.536 5 12.810 3 A/% 8.2 7.5 10.9 11.2 9.6 9.6 9.0 7.8 B 2 056 2 202 2 701 2 610 2 377 2 296 1 950 1 787

下载: 导出CSV

-

[1] 陈海春. 高速公路企业风险管理问题初探[J]. 经济研究导刊, 2011(20): 33-34. doi: 10.3969/j.issn.1673-291X.2011.20.015CHEN Hai-chun. Research on the risk management of expressway enterprises[J]. Economic Research Guide, 2011(20): 33-34. (in Chinese). doi: 10.3969/j.issn.1673-291X.2011.20.015 [2] 刘玉新, 颜如意, 李虹. 论高速公路上市公司财务风险与控制[J]. 交通财会, 2011(12): 20-30, 34. doi: 10.3969/j.issn.1005-9016.2011.12.008LIU Yu-xin, YAN Ru-yi, LI Hong. Study on expressway listed companiesfinancial risk and control[J]. Transport Accounting, 2011(12): 20-30, 34. (in Chinese). doi: 10.3969/j.issn.1005-9016.2011.12.008 [3] 尹翠敏. 高速公路经营企业财务风险预警模型研究[D]. 西安: 长安大学, 2011.YIN Cui-min. Study on the financial risk early warning model for expressway operation enterprise[D]. Xian: Changan University, 2011. (in Chinese). [4] 滕振宇. 低盈利高速公路公司财务风险分析及防范对策研究[J]. 交通财会, 2012(4): 42-46. https://www.cnki.com.cn/Article/CJFDTOTAL-JTCK201204012.htmTENG Zhen-yu. Study on the financial risk and precaution measures for low-profit expressway enterprises[J]. Transport Accounting, 2012(4): 42-46. (in Chinese). https://www.cnki.com.cn/Article/CJFDTOTAL-JTCK201204012.htm [5] 张玲, 杨贞柿, 陈收. KMV模型在上市公司信用风险评价中的应用研究[J]. 系统工程, 2004, 22(11): 84-89. https://www.cnki.com.cn/Article/CJFDTOTAL-GCXT200411019.htmZHANG Ling, YANG Zhen-shi, CHEN Shou. An application of KMV model in credit risk evaluation of public companies[J]. Systems Engineering, 2004, 22(11): 84-89. (in Chinese). https://www.cnki.com.cn/Article/CJFDTOTAL-GCXT200411019.htm [6] 鲁炜, 赵恒珩, 方兆本, 等. KMV模型在公司价值评估中的应用[J]. 管理科学, 2003, 16(3): 30-33. https://www.cnki.com.cn/Article/CJFDTOTAL-JCJJ200303007.htmLU Wei, ZHAO Heng-heng, FANG Zhao-ben, et al. KMV model applied in corporate asset valuation[J]. Management Sciences in China, 2003, 16(3): 30-33. (in Chinese). https://www.cnki.com.cn/Article/CJFDTOTAL-JCJJ200303007.htm [7] 夏红芳, 马俊海. 基于KMV模型的上市公司信用风险预测[J]. 预测, 2008, 27(6): 39-43. https://www.cnki.com.cn/Article/CJFDTOTAL-YUCE200806008.htmXIA Hong-fang, MA Jun-hai. A forecast method of credit risk evaluation of listed companies based KMV model[J]. Forecasting, 2008, 27(6): 39-43. (in Chinese). https://www.cnki.com.cn/Article/CJFDTOTAL-YUCE200806008.htm [8] 高扬敏, 陈红伟, 陈刚. 上市公司信用风险的KMV模型分析[J]. 辽宁工程技术大学学报: 社会科学版, 2009, 11(1): 20-22. https://www.cnki.com.cn/Article/CJFDTOTAL-NLGC200901006.htmGAO Yang-min, CHEN Hong-wei, CHEN Gang. Empirical research on credit risk for Chinas listed companies using KMV model[J]. Journal of Liaoning Technical University: Social Science Edition, 2009, 11(1): 20-22. (in Chinese). https://www.cnki.com.cn/Article/CJFDTOTAL-NLGC200901006.htm [9] 张树强. KMV模型在我国上市公司信用风险度量中的适用性研究[J]. 石家庄铁道大学学报: 社会科学版, 2012, 6(2): 21-26. https://www.cnki.com.cn/Article/CJFDTOTAL-SJTS201202008.htmZHANG Shu-qiang. Applicability study of KMV model in credit risk measurement of listed companies in China[J]. Journal of Shijiazhuang Tiedao University: Social Science, 2012, 6(2): 21-26. (in Chinese). https://www.cnki.com.cn/Article/CJFDTOTAL-SJTS201202008.htm [10] 郭立仑. 我国上市公司信用风险度量——基于KMV模型[J]. 生产力研究, 2012(1): 76-77, 81. https://www.cnki.com.cn/Article/CJFDTOTAL-SCLY202202030.htmGUO Li-lun. Credit risk measurement of listed companies in China based on KMV model[J]. Productivity Research, 2012(1): 76-77, 81. (in Chinese). https://www.cnki.com.cn/Article/CJFDTOTAL-SCLY202202030.htm [11] ODECK J, KJERKREIT A. Evidence on usersattitudes towards road user charges—a cross-sectional survey of six Norwegian toll schemes[J]. Transport Policy, 2010, 17(6): 349-358. [12] ALBALATE D, BEL G. Regulating concessions of toll motorways: an empirical study on fixed vs. variable term contracts[J]. Transportation Research Part A: Policy and Practice, 2009, 43(2): 219-229. [13] 杨琦, 杨云峰. 高速公路资产管理体制改革研究[J]. 中国公路学报, 2009, 22(2): 105-110. https://www.cnki.com.cn/Article/CJFDTOTAL-ZGGL200902018.htmYANG Qi, YANG Yun-feng. Study of reform of expressway asset management system[J]. China Journal of Highway and Transport, 2009, 22(2): 105-110. (in Chinese). https://www.cnki.com.cn/Article/CJFDTOTAL-ZGGL200902018.htm -

点击查看大图

点击查看大图

图(6) / 表(3)

计量

- 文章访问数: 663

- HTML全文浏览量: 140

- PDF下载量: 658

- 被引次数: 0